Over the past few months, car manufacturers have shut down factories, tech products have been delayed, and reports of inflation have permeated the media – all of which can be tied to the heavily publicized global chip shortage. Despite the widespread attention that has been drawn to it, few investors and consumers understand the chip shortage and its implications. Why is there a chip shortage? What is being done about it? What does this mean for the economy?

Understanding The Semiconductor Shortage

Semiconductors, more commonly known as computer chips, are tiny electronic devices that power the functions of an abundance of digital products, from cell phones and smart watches to washing machines and cars.

In a digital world, chips are the lifeblood of production. So, it is no surprise that the global shortage has had a widespread impact. However, the temporary economic roadblock is not to be misinterpreted as a permanent threat to the economy; rather, when viewed from a long-term perspective, it is a signal of growth.

At the start of the pandemic, the global transition to a remote lifestyle led to a sharp increase in the demand for chips. The demand shift began in the consumer electronics industry, as families equipped their homes with enough devices to continue learning, working, and socializing remotely. In the following months, the economic restart outpaced expectations, and durable goods such as cars and home appliances experienced an uplift in demand. Alongside spiking consumer demand came an outsized surge in demand for semiconductors, which were essential to continue production.

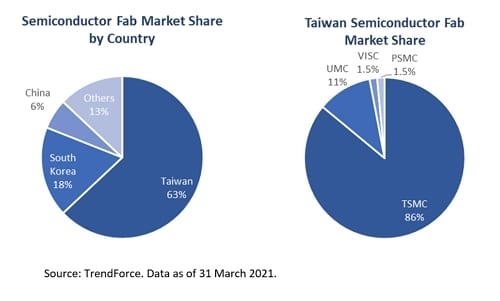

As demand for chips increased, it became apparent that suppliers were not equipped to keep up. Prior to the pandemic, semiconductor manufacturing facilities, known as fabs, were already operating at nearly full capacity and lacked the ability to expand production. Many fabs had shifted production lines to focus on producing modern, “bleeding edge” chips and couldn’t keep up with the demand for the simpler, commoditized chips used in automobiles and appliances. Manufacturing problems were intensified by the lack of geographical diversification among semiconductor fabs. Despite the global need for chips and chip-based products, 87% of semiconductors were produced in Taiwan, South Korea, and China, and the fabrication of 54% of the world’s chips could be traced back to a single entity (Taiwan Semiconductor Manufacturing Company).* A limited supply of chips and an unbalanced market share made a supply chain disruption inevitable.

For chip-reliant companies, the shortage has caused a supply chain bottleneck, forcing many to slow or halt production. Of the industries impacted, the automotive industry has taken the hardest hit, as it has become increasingly reliant on semiconductors. With most semiconductor manufacturers focusing on consumer electronics, automotive companies found themselves at the back of the line for new chips. Many car manufacturers, including Ford Motor Company and General Motors, were forced to shut down plants temporarily. Ford and GM are both expecting to see individual earning cuts of over $2 billion.

The auto industry has not been alone in its struggles amid the global chip shortage. As a result of low output and high demand, the long-awaited Play Station 5 has failed to stay on shelves, leading to significant order delays and the emergence of resale markets. Washers and dryers have also seen production delays and low output, driving prices up and forcing consumers to settle for products that differ from their preferred options.

Blue Chip Partners Outlook

The chip shortage will likely be a short-term headwind for GDP growth. Although semiconductors only directly contribute about 0.3% of the U.S. GDP, they are necessary to produce 12% of the national output. As a result, the supply chain bottleneck is forecasted to cost as much as 1% of 2021 U.S. GDP growth.

Is this harmful to an economic restart?

Not exactly.

In the long-term, the chip shortage may be a signal of economic expansion. A result of rising demand for big ticket items like cars, appliances, and computers, the shortage indicates a rebound in consumer spending. In an economy that is growing increasingly reliant on semiconductor technology, the semiconductor market is likely to become an indicator of overall economic activity, with rising demand for chips suggesting high potential output in related industries.

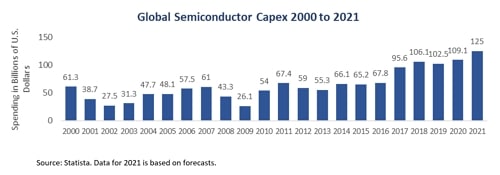

For semiconductor companies, the necessary expansion is already taking place. In order to counteract their low capacity, the “big three” chip manufacturers, Taiwan Semiconductor Manufacturing Co. (TSMC), Samsung, and Intel, have all announced large capital expenditure plans, totaling nearly $150 billion. For TSMC, the world’s largest chip manufacturer, this involves a 47% increase in year-on-year capital expenditures, with subsequent increases expected to follow. Pivotal to the capex plans is a trend to build semiconductor fabs in the southern U.S., with Arizona being a newly targeted hub for chip makers. Both TSMC and Intel have announced multibillion-dollar fab buildouts within the state.

Working alongside these plans are substantial government initiatives that aim to escalate the onshoring of chip manufacturing. Despite accounting for 47% of global semiconductor sales, the U.S. only manufactures about 12% of the world’s chips, making American tech and semiconductor companies reliant on a weakened global supply chain.** The recent U.S. Innovation and Competition Act has allotted $52 billion in funding for semiconductor-related initiatives, which will work alongside Intel and TSMC’s capital expenditure plans to boost U.S. chip production. Not only has the shortage prompted the semiconductor industry to expand, but it also sparked an onshoring trend which will stimulate long-term growth in the American economy.

The U.S. is not the only country working to onshore its semiconductor supply chain. The EU has expressed its need for localized chip makers and has indicated its willingness to form strategic public-private partnerships to fund the initiative. Intel, headquartered in California, is seen as a favorite to expand its production in Europe. South Korea is betting big as well, announcing an investment of over $450 billion over the next 10 years to subsidize the onshoring of semiconductor manufacturing.* The South Korean government plans to provide tax breaks, cut interest rates, decrease regulation, and help fund necessary infrastructure. They will also fund the training of over 36,000 semiconductor experts to maintain their position in the market.

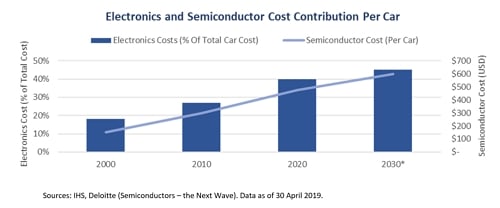

The rapid expansion in public and private semiconductor spending indicates prevailing confidence in the future of the chip industry, as chips continue to become essential inputs in new markets. Of these markets, the Internet of Things (IoT) poses the most intriguing (and financially significant) future. The vision behind IoT – that phones, cars, household appliances, and a myriad other “things” will be able to wirelessly communicate with each other. This assumes that semiconductors will be inputs for the production of a constantly expanding list of products. As IoT expands, semiconductors will grow in demand, and producers will continue to increase production capacity.

Although the current chip shortage has caused an economic disturbance, it is important to remember that high demand is promising, and low capacity is temporary. Semiconductor companies are continuing to expand, and governments are seizing the opportunity to invest in one of the fastest growing industries in the world. Looking past fear-mongering reports and low short-term output, we see that the chip shortage indicates long-term economic expansion.

References:

*https://www.japantimes.co.jp/opinion/2021/06/17/commentary/japan-commentary/taiwan-chip-dependence/

**https://www.businessinsider.com/why-us-doesnt-make-chips-semiconductor-shortage-2021-4#:~:text=Chips%20are%20difficult%20to%20produce,12%25%20of%20global%20chip%20production

Credits

This article was written with the support of the following interns:

Jacob Seabolt

Jacob is a rising sophomore at the University of Michigan Ross School of Business, where he plans to concentrate in finance and minor in creative writing. Having a great interest in finance and analytics, Jacob works in support of Blue Chip Partners’ investment committee to conduct research and track market performance.

Mitch Polich

Mitch is a rising junior with a concentration in Finance at the Eli Broad College of Business at Michigan State University. He utilizes a passion for investments and the financial markets in assisting the investment committee at Blue Chip Partners with equity research.

Expressions of opinion are as of this date and are subject to change without notice. The information provided does not constitute tax, legal, accounting, or other professional advice and is without warranty as to the accuracy or completeness of the information. Any information provided is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation to buy, hold or sell any security. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There are limitations associated with the use of any method of securities analysis. Indices are included for informational purposes only; investors cannot invest directly in any index. Every investor’s situation is unique, and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Past performance does not guarantee future results. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that any statements, opinions or forecasts provided herein will prove to be correct.