The Roth IRA’s Role In Tax Planning

Welcome to the second edition of our series on IRAs. Part 1 discussed the main differences between traditional and Roth IRA accounts.

The Roth IRA, and its cousin the Roth 401(k), can be a powerful tax planning tool in addition to an important retirement savings option. Perhaps the best way to illustrate how you can leverage a Roth IRA or Roth 401(k) in retirement is to show you the real-life tax implications of doing so.

While these scenarios may not reflect the specifics of your personal situation, they can give you an idea of how Roth IRAs work in a real-life situation. They can also help you understand the tax implications of funding a Roth IRA or Roth 401(k) before retirement and withdrawing and spending those assets in retirement.

We hope this information sparks your thinking about how a Roth IRA or Roth 401(k) may be able to help you reach your retirement goals. As always, our advisors are available to discuss your specific situation and answer your questions.

Taxes: Now Or Later?

The most compelling feature of the Roth IRA and Roth 401(k) is that withdrawals from these accounts are not taxed as long as you are at least age 59-1/2 and you have had the account for at least five years. However, the amounts you contribute to these accounts are not tax deductible. This is the opposite of how withdrawals from a traditional IRA or 401(k) are treated, with contributions tax deductible and withdrawals fully taxed as income.

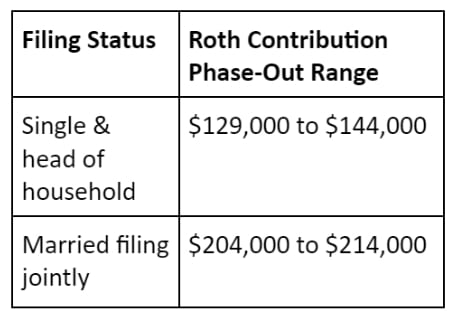

In addition, not everyone is eligible to fund a Roth IRA, depending on the modified adjusted gross income (MAGI) on their tax return. For most taxpayers, this will be your adjusted gross income. As the table below shows, the ability to contribute to a Roth IRA starts to phase out when your MAGI reaches the lower end of these income ranges and is eliminated completely when you surpass the high end of these income ranges.

It is important to note that these MAGI ranges apply only to Roth IRA contributions. There are no income limits on making Roth 401(k) contributions.

Does Funding A Roth IRA Or Roth 401(k) Make Tax Sense?

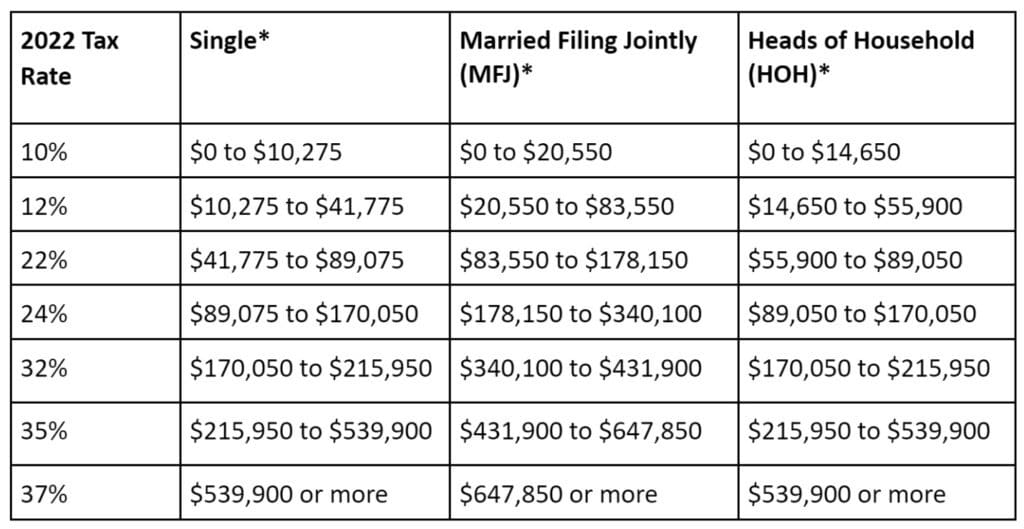

Even if you meet the MAGI requirements to make a Roth contribution, that does not automatically mean that it makes sense to do so. Keeping in mind that Roth IRA and Roth 401(k) contributions are not tax deductible, you can use the following table to get a sense of the tax “cost” of making Roth contributions instead of traditional tax deductible IRA or 401(k) contributions using tax rates for 2022.

*The income amounts presented in this chart represent taxable income. Taxable income is adjusted gross income minus the standard deduction minus charitable contributions and the qualified business income deduction. Ask your accountant or Blue Chip advisor for more information.

The following examples use these tax rates to show the tax implications of making Roth IRA or Roth 401(k) contributions during your working years or withdrawing assets from a Roth IRA or Roth 401(k) during retirement.

Examples Of How Tax Implications Of IRAs Work:

Establishing A Roth IRA: Jim, Age 33, Single

Jim’s MAGI for 2022 is $87,500, primarily comprised of W2 wages. Jim can make pre-tax retirement contributions through his employer’s 401(k) plan, but he also wants to contribute to a Roth IRA to get tax-free investment growth.

Eligibility: Because Jim’s MAGI is below the $129,000-$144,000 phase-out range for single taxpayers AND his earned income is more than $6,000, Jim can contribute the full $6,000 to a Roth IRA for tax year 2022.

Tax impact: Jim is in the 22% marginal tax bracket and any Roth IRA contribution is not tax deductible. Therefore, by choosing to make a Roth IRA contribution, Jim will be paying $1,320 more in taxes ($6,000 contribution x 22% tax bracket) than he would if he chose to make a tax-deductible traditional IRA contribution. However, any earnings on this and any other Roth IRA contributions Jim makes can be withdrawn tax-free in retirement.

Roth IRA For Stay-At-Home Parent: Tina (37) and John (35), Married Filing A Joint Tax Return

Tina works outside the home and John stays home to care for their two young children. Their MAGI is $200,000 for 2022 and Tina contributes to her employer’s 401(k) plan. Even though John is not currently employed, he would like to start putting money away for retirement.

Eligibility: John’s eligibility for Roth IRA contributions depends on the couple’s MAGI and earned income. In this case, the couple’s income is low enough to allow John to make a full Roth IRA contribution. John is able to make a contribution even though he himself does not earn income because John and Tina file a joint income tax return and Tina’s income is at least $6,000.

Tax impact: John’s Roth IRA contribution is not tax deductible. However, any earnings on this contribution and future contributions can be withdrawn tax-free.

Taking Advantage of a Roth 401(k) Option: Rick (46) and Leslie (45), married filing a joint tax return

Rick and Leslie are ineligible to contribute to a Roth IRA because their combined MAGI for 2022 of $230,000 exceeds the income limits for these contributions. However, they want to explore other options.

Eligibility: Acting on the advice of his financial advisor, Rick asks his company’s HR department about making Roth contributions to his 401(k) account and finds out that the plan allows both traditional pre-tax and Roth contributions.

If Rick decides to make both pre-tax and Roth contributions to his 401(k) plan, he can choose any mix between the two as long as the total of those contributions is not more than the IRS limit for his age (currently $20,500).

When Rick turns 50, he will be able to make additional “catch-up” contributions (pre-tax or Roth) to his 401(k) account of up to $6,500 per year.

Tax impact: Rick’s Roth contributions to his 401(k) account will be included in his W2 wages and must be reported as taxable income on his and Leslie’s joint tax return. The investment growth in the Roth portion of his 401(k) account will not be taxable when Rick is eventually able to withdraw the money, exactly like a Roth IRA.

If Rick were to contribute the maximum to his 401(k) account using only the Roth option, he would pay $4,920 [$20,500 x 24% tax bracket] more in taxes than if he chose to make pre-tax (i.e., tax deductible) 401(k) contributions. If he chooses the Roth option to make “catch-up” contributions when he turns 50, the total Roth contribution (regular and catch up) would total $27,000 and the tax impact of choosing Roth contributions rather than pre-tax contributions would total $6,480 [$27,000 x 24% tax bracket].

If Rick chooses to make $6,000 in Roth contributions and $14,500 in pretax contributions, he would pay $1,440 [ $6,000 x 24% tax bracket ] more in taxes than if he chose to make all of his 401(k) contributions on a pre-tax (i.e., tax deductible) basis.

In both cases, all pre-tax 401(k) contributions and growth would be taxed as ordinary income when withdrawn in retirement and all Roth 401(k) contributions and growth would be withdrawn tax free.

Managing Distributions: Sandy (68), Retired And Single

Sandy is retired from her job and considering how to manage distributions from her traditional IRA and Roth IRA during her retirement. Her pension and Social Security income provide $45,000 in taxable income for 2022, which is enough to pay for her core expenses. However, Sandy needs to replace her roof at an estimated cost of $15,000. To pay for this, Sandy will need to take a distribution from one of her retirement accounts.

Tax impact: The tax impact of this distribution will differ greatly depending on whether she chooses to take the $15,000 from her traditional IRA, Roth IRA or a bit from both.

If Sandy takes a distribution from her traditional IRA, she will have to report this amount as income on her tax return. In fact, she will have to increase the total amount of the withdrawal to ensure she has enough money to cover the taxes on that distribution. Because she is in the 22% tax bracket she will need to withdraw the $15,000 for the roof plus another $4,230.77 to “gross up” the full amount to cover these taxes for a total of $19,230.77.

If Sandy takes a distribution from her Roth IRA, she will only need to withdraw $15,000 because such withdrawals are tax free in retirement.

Managing taxes in retirement: Arnie (80) and Carol (76), married filing jointly

Arnie and Carol are expecting a large amount of taxable income in 2022 from several sources. Both are over age 72 so they must make required minimum distributions (RMDs) totaling $125,000 from their large traditional IRA accounts. This, combined with their income from other sources, has led to a level of taxable income that far exceeds their $75,000 in annual expenses and is likely to result in taxes on 85% of their Social Security benefits.

“What if” tax scenario: In a situation like this, it is interesting to see how the tax impact of this scenario would change if Arnie and Carol had some money in a Roth IRA or Roth 401(k).

For example, if Arnie and Sandy both had 25% of their retirement assets in Roth IRAs, the RMDs from their traditional IRAs would be reduced from $125,000 to $93,750 in 2022 and they would save $6,875 in taxes [ $125,000 – $93,750 = $31,250; $31,250 x 22% tax bracket = $6,875 ]. Roth IRAs and Roth 401(k)s do not have RMDs and their assets can be withdrawn in retirement tax free.

Is The Roth IRA Or Roth 401(k) Right For You?

As these examples show, everyone’s financial situation is unique. If you have any questions related to Roth IRAs or Roth 401(k)s and your particular income and tax circumstances, please reach out to a Blue Chip advisor. We are here to help.

Read more about Roth IRAs here.

Expressions of opinion are as of this date and are subject to change without notice. The information provided does not constitute tax, legal, accounting, or other professional advice and is without warranty as to the accuracy or completeness of the information. Any information provided is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation to buy, hold or sell any security. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There are limitations associated with the use of any method of securities analysis. Indices are included for informational purposes only; investors cannot invest directly in any index. Every investor’s situation is unique, and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Past performance does not guarantee future results. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that any statements, opinions or forecasts provided herein will prove to be correct.