As we digest the state of U.S. markets today, here are the details on the three key themes to watch in the fourth quarter of 2021:

You’re Hired!

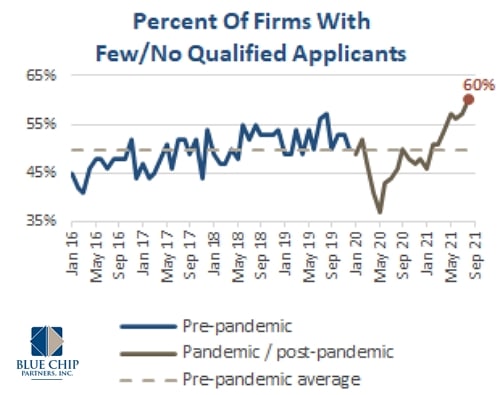

From an economic perspective, the United States has proved resilient. After GDP growth of an annualized 6.5% in the second quarter, the U.S. economy is now larger than it was before the pandemic. Strong household balance sheets have fueled robust consumer spending, a trend we highlighted last quarter and one that we see persisting. There is, however, a formidable chink in the economy’s armor; it is nearly impossible to hire individuals.

This is especially pertinent for small businesses, the backbone of the U.S. economy. A record number of small businesses have open positions which they are unable to fill, leading to constraints on operating hours and capacity. With the labor participation rate at 61.7% vs. 63.3% pre-COVID, the dynamics at play are clearly hindering the next leg of this economic restart. As the Delta variant made a noticeable impact on job growth in the back half of the third quarter, some combination of a general fear of the virus and desire for more workplace flexibility is leading individuals to take their time with returning to the workforce.

Going forward, there is potential for hourly earnings (up 4.3% y/y as of the end of August) to continue to march higher as the balance of power remains with potential employees. In the immediate-term, we are intently watching to see if the September withdrawal of excess unemployment benefits can successfully lead to the filling of some of the record-high 10.1 million open jobs. Any reduction in that eye-popping number would be helpful in keeping a lid on wage inflation.

Equities In Charge

At Blue Chip Partners, we are rooted in the belief that given a long-term time horizon, an overweight allocation to equities is prudent. When viewing rolling 10-year equity returns, very few periods in history would have yielded a negative result.

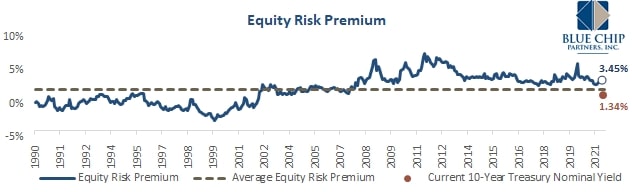

Further, today’s environment for traditional interest-bearing securities is rather dull, as investors currently experience negative real yields across a large portion of the fixed income market (real yield = bond yield after expected inflation is considered). Today, investors are essentially paying to participate in “risk-free” treasuries and are earning less than a high yield savings account in prime-rated corporate bonds.

On the equity side, it appears that investors are set up to be more favorably rewarded relative to the level of risk involved. The Equity Risk Premium (ERP) provides insight into whether or not equity market participants are properly compensated for assuming additional risk in stocks relative to “risk-free” government bonds. The ERP has resided above its long-term average post-2008 financial crisis, and remains elevated today.

This suggests that stocks remain undervalued from the standpoint of risk vs. potential reward.

For another valuation angle, read the full report attached below.

The Road Ahead

While our outlook for the economy and financial markets is constructive, you may recall that our Q3 Quarterly Edge pointed out the tendency for the second year of a secular bull market to pose bumps in the road. We have digested elements from the last quarter that should be reassuring to investors, but as with any market environment, risks appear on the horizon as well. A summary of potential catalysts, positive and negative, are outlined below.

Bullish Observations

Cash on the sidelines:

While everything from semiconductors and personal electronics to washing machines and couches are in short supply, the same cannot be said for cash. The level of liquidity on both personal and corporate balance sheets has never been higher, which provide a base for an optimistic equity market outlook.

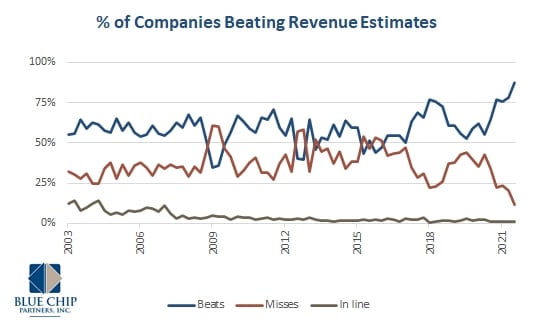

U.S. businesses have proven themselves:

It is encouraging to see that a record number of firms are posting financial results that are above consensus expectations. Businesses have weathered the challenging environment that arose post-pandemic, and we believe there are ample examples of companies who are poised to continue to execute well.

Potential Risks

Margin degradation:

Earnings have been the primary driver of returns in 2021. However, supply chain challenges have persisted, and if wage pressures accelerate due to continued labor shortages, less resilient businesses will be exposed. Margin degradation is not our base case, but it highlights the need for selectivity.

Policy push:

With a smattering of potential policy actions on the horizon, markets may be susceptible to headline risk in the coming quarter. Infrastructure negotiations, Fed tapering and reappointments, and the debt ceiling all will garner attention from investors, although President Biden’s fiscal policy may be the most impactful. Tax hikes would certainly impact corporate bottom lines, and it remains to be seen if investor sentiment will be affected.

Your Bottom Line

The U.S. economy has proved resilient after the bumps in the road presented by the COVID-19 pandemic. Data points to continued growth through the end of the year, albeit with lower intensity than has been seen through the first three quarters of 2021. The employment picture remains the laggard, as a stubbornly low participation rate could lead to continued upward pressure on wages. Small businesses are feeling the pain given the lack of available labor, a trend that we hope to see moderate over the next six months as virus fears moderate and excess unemployment benefits are withdrawn.

While the fixed income market poses unique challenges via ultra-low interest rates and deteriorated purchasing power, equities appear ripe for investment today. Earnings growth at the company level has outpaced price appreciation, which has led to multiple contraction and thus more attractive valuations on a price-to-earnings basis. Further, the Equity Risk Premium, which sheds light on the attractiveness of stocks relative to government bonds, remains well above the historical average. This indicates that investors are more than fairly compensated for the assumption of additional risk in equities relative to fixed income.

The road ahead finds financial markets at an interesting juncture. We find optimism in a tremendous amount of corporate and individual cash on the sidelines as well as a record number of companies posting financial results that exceed already lofty expectations. On the contrary, potential risks on the horizon solidify the need for selectivity in markets. There is potential for companies to experience margin pressure amid rising labor costs and supply chain challenges, and a host of high-profile political items may lead to wavering investor sentiment.

View more Blue Chip Quarterly Edge updates here.

Expressions of opinion are as of 30 September 2021 and are subject to change without notice. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Every investor’s situation is unique, and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Past performance does not guarantee future results. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that any statements, opinions or forecasts provided herein will prove to be correct.