Market Outlook

Returns experienced by investors in U.S. markets in Q2 2024 were meaningfully different than those seen in the first quarter. In Ql, the S&P 500 Index provided a double-digit return, the average S&P 500 stock advanced at a high-single-digit clip, and bond market returns ended in negative territory. In Q2, the concentration of returns seen in 2023’s equity market was again evident. Specifically, the S&P 500 Index posted a mid-single-digit return, but the average S&P 500 stock settled firmly in the red. The bond market found a bottom and charged higher before it ultimately ended the quarter flat. With two quarters of starkly different performance profiles thus far in 2024, what should be top of mind for investors in Q3 and beyond?

Recent economic softness and the upcoming U.S. presidential election will be in focus. While we remain optimistic with regards to a full-year outcome for financial markets, investors should expect volatility on the back of middling economic readings and a ramping election cycle.

With regards to bonds, we maintain our belief in the value that the fixed income market currently offers relative to cash assets, and the volatility-inducing elements cited above further support our constructive view.

In the equity market, we find it imperative for investors to think critically about the artificial intelligence “hype cycle” that is being experienced at current.

Is a Midsummer Storm Brewing?

Bonds: Don’t Miss the Boat

The AI Hype Train: Choose the Right Seat

Your Bottom Line

We see room for persistence of the recent trend in economic data, and anticipate election-driven volatility through the summer months. Indicators point to economic slowness, and while history shows stock momentum has continued following a positive start in an election year, data also supports the potential for higher volatility in the coming months.

Attractive yields, an economic slowdown, and election-driven volatility support bonds. Regardless of action from the Federal Reserve, bonds appear in a position to add value to investor portfolios via income, capital appreciation, and volatility mitigation.

Excitement for artificial intelligence has created trillions of dollars in market capitalization – avoid previously seen mistakes. Al-related stock movement has not necessarily been accompanied by consummate earnings growth. While perhaps not imminent, consolidation, competition, and estimate revisions are likely on the horizon. Consider accessing the theme through companies that are indirect beneficiaries of the scaling of artificial intelligence.

Is a Midsummer Storm Brewing?

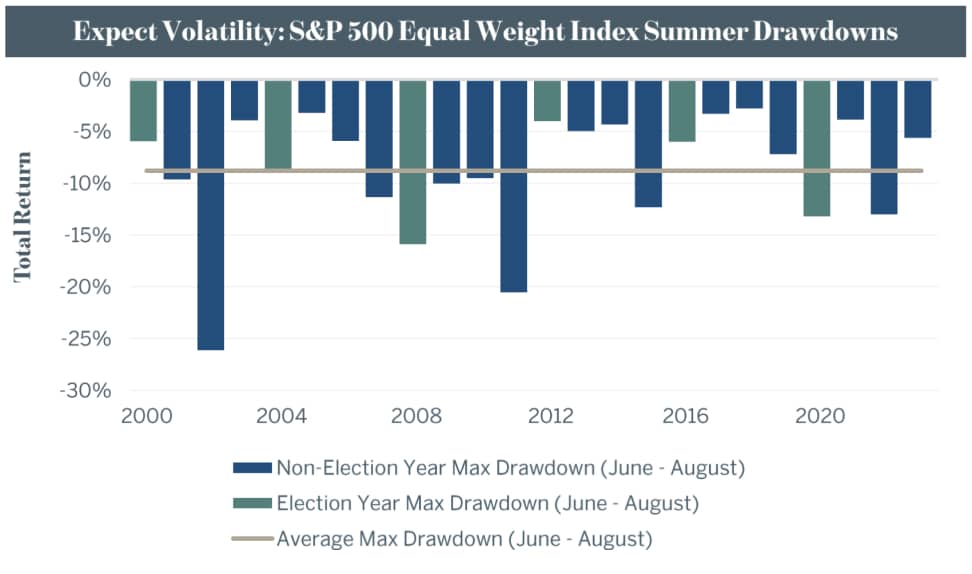

If you read our analysis of stock market returns in U.S. presidential election years, you will recall that elections in and of themselves have no observable impact on calendar year performance. They do, however, generally stoke elevated volatility in equity markets through the summer months as the election comes into focus. With the June – August period historically being a weak period, layering in an election and a softening economy is likely to result in a choppy experience. Slower consumer spending, weakening job growth, and rising layoffs are all observable today, which supports our expectation for above average volatility in the coming months. Since 2000, the average max drawdown for the S&P 500 Equal Weight Index between June and August is -8.81 %. In election years over the same period, the max drawdown has been roughly the same, -8.95% on average. To be clear, we aren’t calling for a decline in equity markets through year-end. 2008 is the only election year over the last 20 years in which the domestic equity market printed a negative calendar year return. The same is true for a condensed performance period from June through the end of each election year since 2000. Rather, we simply assert that as emotionally charged trading takes hold and the underlying economic trajectory develops, expect bumpiness in the stock market.

Bonds: Don’t Miss the Boat

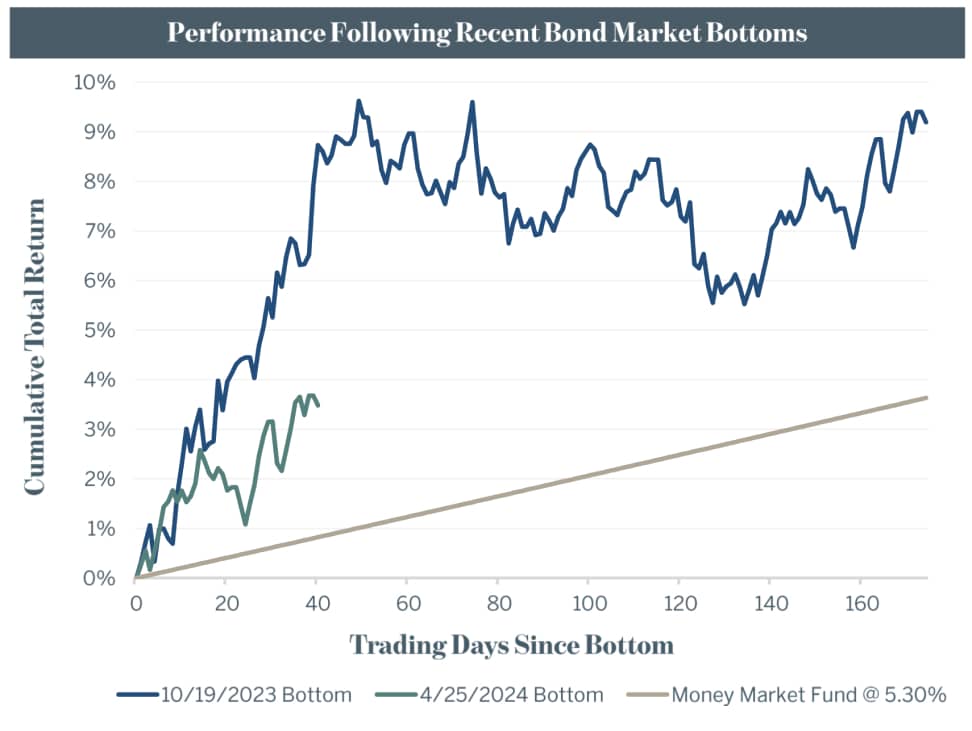

We continue to be supportive in our outlook for the bond market. The themes we outlined in our Q2. 2024 Quarterly Edge and prior materials remain as underpinnings, and the elements noted above with regards to the economy and the election serve to increase the attractiveness of traditional fixed income in our view. The direction of interest rates as influenced by the Federal Reserve will remain uncertain, but as we have discussed in the past. waiting for outright changes in the baseline interest rate is a losing proposition from a return perspective. Financial markets are forward looking, and thus bond market participants will push prices upward well before the Fed enacts reductions in the Fed Funds Rate. Said another way, it is better to be early than late in our view, especially as highquality segments of the fixed income market offer a level of annual income that is competitive to cash assets (such as money market funds). The Bloomberg US Aggregate Bond Index is negative year-to-date as of this writing, meaning that investors that have sat in cash have not yet missed the boat. However, it is worth noting that moves in the bond market can happen quickly, which further supports our preference for being early than late (and getting paid while you wait). Take the example below, which outlines the bond market’s move off the two most recent bottoms. We see downside in the traditional fixed income market as limited from here, while the opportunity cost of remaining heavily allocated to cash looms large.

The AI Hype Train: Choose the Right Seat

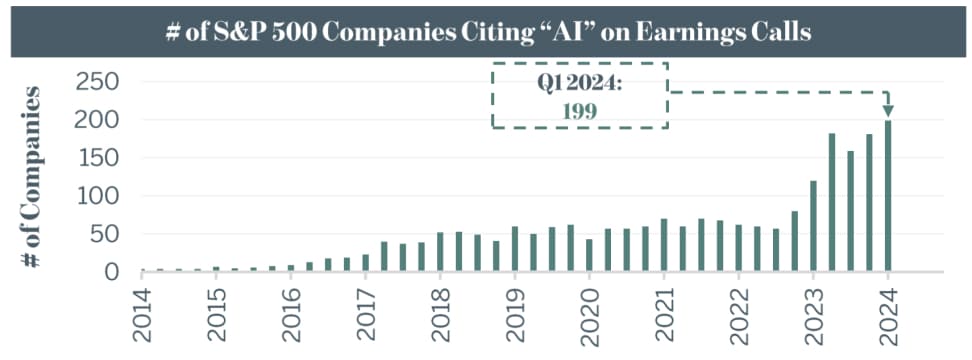

Arguably the most high-profile theme in public markets over the past two years, the “hype” around artificial intelligence continues to charge higher. One can observe this hype by way of the number of companies that reference “Al” on their corporate earnings calls, which has increased nearly 4x in just two years. In Ql 2024, the term was mentioned at least 50 times each on the earnings calls of 12 S&P 500 companies, led by Meta Platforms Inc. (95), NVIDIA Corp. (86), and Microsoft (74).

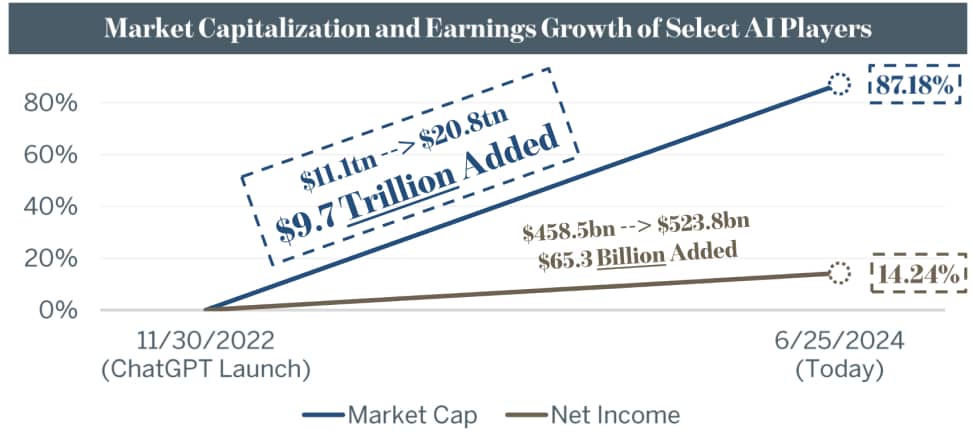

The hype is also observable via the market capitalization created by expectations for the financial impact of artificial intelligence, Using the holdings of the WisdomTree Artificial Intelligence and Innovation Fund as a proxy, a select list of companies that are primarily involved in the themes of Al and innovation have collectively added $9.7 trillion (87.2%) in market cap since the launch of ChatGPT in November 2022. The growth experienced has not been reflective of consummate earnings expansion, but proponents would base their argument on future expectations for the earnings impact of Al. What happens if current expectations are incorrect?

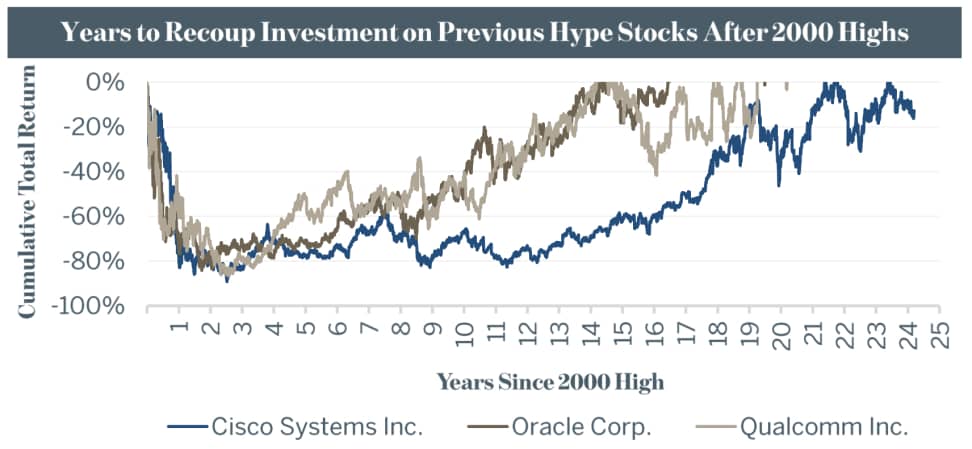

The pessimistic “what-if” scenario has already been experienced. Look to darlings of the Tech Bubble for reference, such as Cisco Systems Inc., Oracle Corp., and Qualcomm Inc. The rapid growth of the internet, new business models, and media hype (along with investor FOMO – fear-ofmissing-out) catapulted expectations for future profitability. From a business perspective, the results of the various innovations in the period were impactful, just not to the degree that initial prospects would have pointed to. Unlucky investors that bought into these three stocks at the top in 2000 would have waited almost two decades for a positive return, with shares of Cisco now back below the high experienced in 2000.

Our language above should not be perceived as a pessimistic stance on artificial intelligence broadly. The potential for gains in efficiency and productivity spurred by Al are truly staggering and stand to benefit both consumers and corporations across all sectors. Instead of allocating to the well-known, massively hyped names in the equity market, we recommend looking one layer deeper to identify firms that are poised to benefit, but which are not overleveraged to the theme itself.

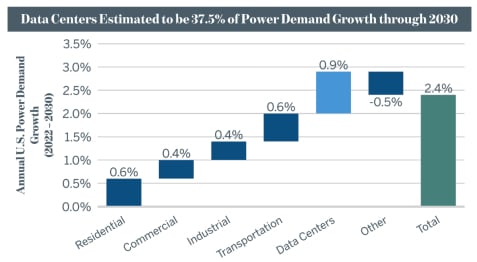

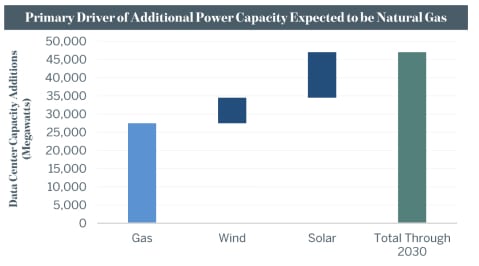

As an example, artificial intelligence requires an immense amount of data, which in turn prompts a need for additional data center storage capacity. Data centers are among the most energy-intensive buildings which means if Al is to scale as expected, the U.S. needs to invest significant resources into additional power capacity. The knock-on beneficiaries of an Al-driven power consumption thesis are found across industries (not just tech), and although these companies would benefit from higher corporate and government spending on Al, they are not solely reliant on the story to exhibit value. Beneficiaries from higher demand growth include companies such as utilities, renewable energy providers, turbine manufacturers, and energy storage players – all of which possess reliable streams of revenue growth outside of the Al catalyst. Also in play are supply chain / infrastructure beneficiaries, such as firms that provide power transmission and distribution networks as well as those that focus on the build out and reliability of the grid. Instead of gambling in hopes of identifying the one Al enabler that wins out, we believe that indirect beneficiaries that are poised for success even if spending on the theme falls short can be a more prudent approach to investing in artificial intelligence.

Disclosures

Expressions of opinion are as of 30 June 2024 and are subject to change without notice. Any information provided is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation to buy, hold, or sell any security. There are limitations associated with the use of any method of securities analysis. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Every investor’s situation is unique, and you should consider your investment goals, risk tolerance, and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Past performance does not guarantee future results. Investing involves risk, and you may incur a profit or loss regardless of strategy selected. There is no guarantee that any statements, opinions, or forecasts provided herein will prove to be correct. Dividends are not guaranteed and must be approved by the company Board of Directors. Indices are included for informational purposes only; investors cannot invest directly in any index.

Market Outlook: Source: Bloomberg Finance L.P. As of 30 June 2024. The average S&P 500 stock refers to the S&P 500 Equal Weight Index and the bond market / bonds are represented by the Bloomberg US Aggregate Bond Index. Past performance does not guarantee or indicate future results. Index performance is for illustrative purposes only. It is not possible to invest directly in an index.

Expect Volatility: S&P 500 Equal Weight Index Summer Drawdowns / S&P 500 Equal Weight Index Returns (2000 – 2020): Source: Bloomberg Finance L.P. As of 30 June 2024. Data shown is representative of the S&P 500 Equal Weight Index from 31 May to 31 August for each calendar year between 2000 and 2020, or for the full calendar year where indicated. Index performance is for illustrative purposes only. It is not possible to invest directly in an index.

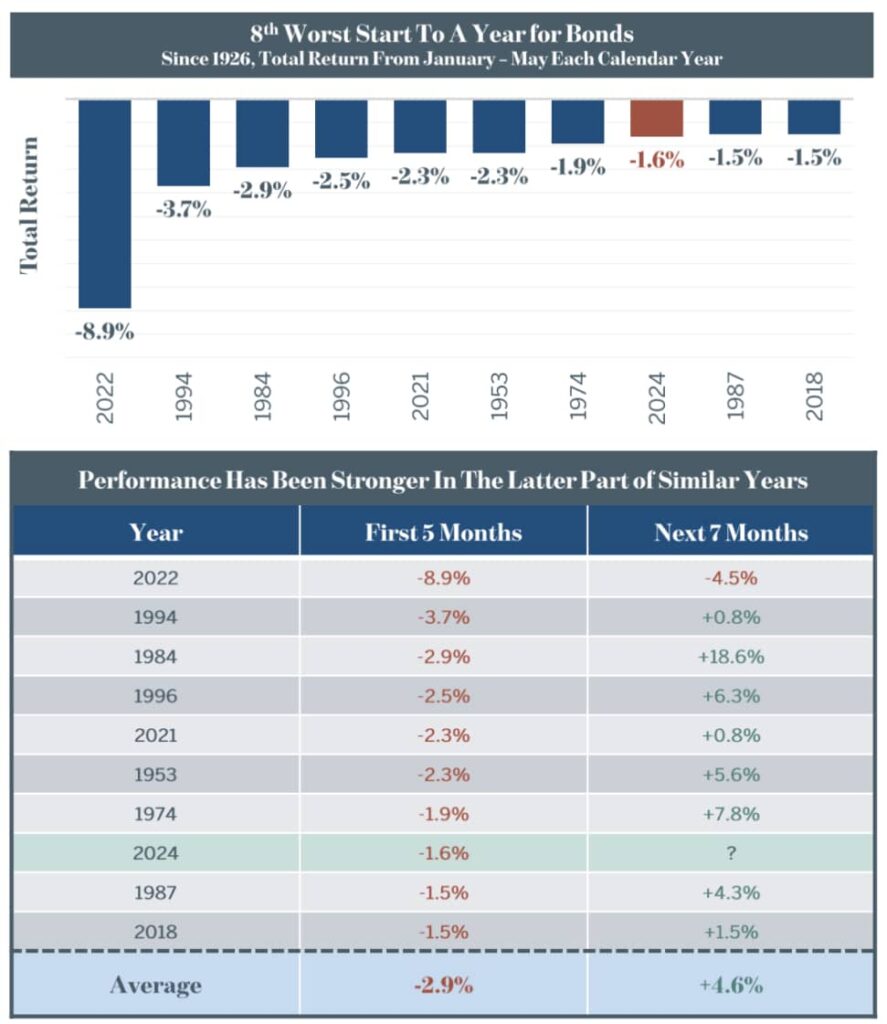

8th Worst Start To A Year for Bonds / Performance Has Been Stronger In The Latter Part of Similar Years:

Source: BlackRock with data from Morningstar. As of 31 May 2024. U.S. bonds represented by the IA SBBI US Gov IT Index from 1/1/26 to 1/3/89 and the Bloomberg US Aggregate Bond Index from 1/3/89 to 5/31/24. Past performance does not guarantee or indicate future results. Index performance is for illustrative purposes only. It is not possible to invest directly in an index.

Performance Following Recent Bond Market Bottoms: Source: Bloomberg Finance L.P. As of 20 June 2024. Bonds are represented by the Bloomberg US Aggregate Bond Index. Money Market Fund @ 5.30% assumes a 5.30% annualized return, or a 0.0204954465185203% daily return. Index performance is for illustrative purposes only. It is not possible to invest directly in an index. # of S&P 500 Companies Citing “Al” on Earnings Calls: Source: FactSet. As of 24 May 2024. The S&P 500 Index is a market capitalization weighted index that tracks the performance of 500 of the largest companies that are listed on stock exchanges in the United States. Data shown is reflective of the number of companies that cited “Al” during each quarter’s corporate earnings calls.

Market Capitalization and Earnings Growth of Select Al Players: Source: Bloomberg Finance L.P. As of 25 June 2024. Select Al Players refers to companies held by the WisdomTree Artificial Intelligence and Innovation Fund. Excludes Arm Holdings pie as the company was not publicly traded on 11/30/2022. Net Income as shown refers to trailing 12-month net income.

Years to Recoup Investment on Previous Hype Stocks After 2000 Highs: Source: Bloomberg Finance L.P. As of 24 June 2024. 2000 highs are reflective of the following dates – CSCO: 27 March 2000, ORCL: 1 September 2000, QCOM: 3 January 2000.

Data Centers Estimated to be 37.5% of Power Demand Growth through 2030: Source: Goldman Sachs Global Investment Research and the U.S. Energy Information Administration. As of 28 April 2024. Data shown is reflective of estimates for the composition of and total annual U.S. power demand growth from 2022- 2030.

Primary Driver of Additional Power Capacity Expected to be Natural Gas: Source: Goldman Sachs Global Investment Research. As of 28 April 2024. Data shown is reflective of estimates for the sources of data center driven power capacity growth in the U.S. through 2030. Copyright© 2024. All rights reserved.